New:

Selected LAW School abuses

* ThirdTierReality.Blogspot.com (Blog's goal is to inform potential law school

students & applicants of the ugly realities of attending law school.)

* InsideTheLawSchoolScam.Blogspot.com

* LawSchoolTuitionBubble.Wordpress.com (Research & commentary on

the Law School Tuition Bubble.)

* SubPrimeJD.Blogspot.com (A blog dedicated to exposing the law school & higher education

scam, the 'Ponzi-like' structure of the US economy and in opposition to the US war machine.)

* ForgottenAttorney.Wordpress.com (A voice among the silent majority of young

attorneys.)

* FirstTierToilet.Blogspot.com (Just Another Blog by an Indignant Graduate for

Indignant Graduates.)

* TemporaryAttorney.Blogspot.com (With over 5,000 daily visitors, help expose the

nasty sweatshops, swindling law schools, and opportunistic staffing agencies.)

* http://CenterForCollegeAffordability.org (Founded in 2006, The Center for

College Affordability and Productivity (CCAP) is an independent, not-for-profit research center based in Washington, DC. The CCAP exists to help

facilitate a broader dialogue on the issues and problems facing the institutes of higher education in the United States. Currently, their research agenda

includes the following areas: Student Financial Aid Policy; Rising Costs of College; Causes of Higher Education Inefficiencies; Productivity of Staff

and Faculty Members; For-Profit Higher Education; and, Accreditation Old

Blog: CollegeAffordability.Blogspot.com)

Higher-Ed Tuition Costs: The ‘Conservative’ view is not on either extreme Students are told from an early age that an education is the only way to success, and yet when they follow the inevitable path, they are lured

into a trap -a debt-trap.

By Gordon Wayne Watts (Editor-in-Chief: The Register -- GordonWatts.com / GordonWayneWatts.com)

(A 377-word Letter on this same topic [link /

cached copy 1 /

cached copy 2] published Sunday, Oct. 18, 2009 in The Tampa Tribune, Views section,

p.3.;and, a 295-word Letter on this same

topic [link /

cached copy 1 /

cached copy 2] published Friday, June 03, 2011 in The Ledger (of LAKELAND, Fla.),

Editorial page, p.A8. -- Published: Monday, 28 September 2009 ;Last Modified: Sunday, 20 January 2013 NOTE: This short, well-documented research paper (which has been cited[39] in Wikipedia's articles, as well

as The Whitehouse Petitions link here) is only 2,095

words (13,131 characters), according to OpenOffice Word Processor -- Titles, Headers, Updates, Graphs, & citations to Sources (to document some strong claims herein) drive the word-count up considerably,

but The Register does not stop short to cite our sources.

Position Paper -- A well-documented study into the U.S. Higher Ed crisis: Causes of skyrocketing tuition and declining quality of institutions of Higher Education

in America -- Proposed solutions

We think of conservatives as right extremes & liberals as left, polar opposites. However, true conservatives are in the middle (on this matter anyhow), liberals on the

extremes. First, the history:

In the 1956-57 school year, one source[1] reports a year of college cost $138, and another source[2] is in close agreement. But remember we have to adjust for inflation: The $138 figure is about $1,062.71 in 2008 dollars[7], probably the same for 2009, considering the year’s inflation[3] was about 0.1%. However, nowadays, the same year of college costs about $10,066, about a 10X increase. Other sources[4-6] indicate a cost of $6,142.58 for tuition and $6,920.94 for housing, for a total of $13,063.52 per year, even higher than the $10,066 fig.

Drug users and the criminally insane can take out a line of credit, and run up tons of debt and (although it's hard) still declare bankruptcy.[8-11;36] However, student loans are unique

among all loans in the lack of standard consumer protections (truth in lending; bankruptcy proceedings; statutes of limits; the right to refinance; adherence to usury laws; and, Fair Debt & Collection

practices, etc.) afforded the borrower.[12-14] (If institutions of Higher-Ed knew that students could declare bankruptcy, they would be more apt to charge a fair, free-market value for their product

-instead of monopoly-style collusion to keep both tuition principle as well as interest rates[36] high -with garnishment and collection and powers that a mobster would envy.)

The fact that this has driven many students to suicide[15-18;36] is not without merit: You used to never hear of student loan suicides -this has only now become a crisis in Higher-Ed recently. (Their blood should count for something.) OK, that’s the problem: Skyrocketing Tuition & ‘Tuition Bankruptcies,’ like ‘Medical’ & ’Housing Bankruptcies.’ If Education is the BACKBONE of America, we have a BROKEN BACK. However, have you considered why this has only now occurred? Let’s eliminate higher quality as an explanation for the tuition increase. Mainstream media[19-21] claims education quality has actually decreased; Sean Hannity & I both agree[22] that quality has plummeted, so higher tuition isn’t due to better quality.

Any guess why skyrocketing tuition increases have only NOW become a problem? Yes. Since government keeps bailing out[Figure-3] Higher-Ed with our tax dollars[Figure-2] for grants & loans to students and funding of colleges & universities, these institutions have guaranteed income, thus no incentive to lower prices to Free Market supply & demand values. Put another way, they could care less if you go bankrupt & screw-up your life trying to pay off your debt: They’ve already gotten bailed out[Figure-3] in advance. Picture this: Let’s say every restaurant & supermarket is subsidized by Big Brother using tax dollars: Would they be hurt if they charged say $100 for a Big Mac, eventually bankrupting you? No. This isn’t the first time the concept of either expensive food[23] or over-taxation[24] has surfaced. Same with Higher-Ed, the Housing Market, and Social Security. Because of inefficiency & graft, both Hannity & I also agree[22][Figure-2] that tax dollars don't need to keep going to Higher-Ed: Let them stand or fall on their own merit -free market style.

It seems that every time Congress raises the loan limits for Student Loans, and students can afford more (read: go deeper in debt), colleges mysteriously find new excuses to raise the

tuition. "Things that make you go 'hmm...'."

Here's where I break ranks with Sean: He feels no matter what government throws at us, we can somehow pay off bills if we work hard from 6am-midnight.[22] NOT. Here's where liberal extremes come in:

* On one extreme: You have people asking for free handouts. They don’t want to pay for ANY education: Let the government do it all: That's how Sean classed me in his recent show.[22]

* On the other extreme: You have today’s students paying MORE than their fair share, FAR more than peers of yesteryear, for an education whose quality has actually gone DOWN, not up. Since most colleges & universities are state-owned & state-funded and practically ALL institutions of higher ed, even private colleges, receive funding from tax dollars[Figure-2] through grants & loans (not to mention being tightly regulated by government as well), they're a de facto ARM of government. Thus funding influx (e.g., tuition) is effectively a tax by the very definition. And if you have someone like Hannity defending extortion of students by a tax[22] which has already increased 10X, you're effectively supporting tax increase.[24] This extreme is also "Blue-State"-liberal.

Therefore, having each student owe only the actual value of his/her education would be the conservative thing to do[Figure-1] because it falls under moral rights & wrongs as a right

thing. Jesus even asked followers[25] that if someone wanted you to go 1 mile to go 2 (e.g., ‘double’). So there's a good case to be made that paying ‘DOUBLE’ (that is, 200%) is also OK since many fiscal

conservatives are also religious conservatives thus in alignment with Jesus’ creed. Society has finally gotten rid of the scourge of slavery[26] -or have we[38]? Now they've found a way to snare a whole new

group: "Debt Slaves"[26-27,38] of all races, creeds, and genders -who they would put in bondage for life under crushing debt. So, immediate forgiveness of the debt[28] of those overcharged would be the

only way to right the wrongs and then reset the debt owed to 100%-200% of actual costs. For those who've already somehow paid back their debt, this is stickier. Either these students would have to forgive

the government or they might get free education for family members, but to outright refund them cash, even if morally justified, might have an extreme inflationary effect as the number of dollars in

circulation increases. Besides being the morally "right" thing to do, when these debt slaves[26-27,38] are freed, they will be able to spend more money on basic necessities -thus stimulate the economy; the

only ones who would suffer are the banks and lenders -who profit off of others' financial ruin. Colleges made do in the past & they'd make do now to learn to live within their means, stop paying

exorbitant salaries, funding stupid building projects, unnecessary clubs & activities.[33] We’ve done it before -we must do it again: "Red-State"-Conservatives must once

again save the future.(PS: If you’re a liberal reading this, you should realize that this affects you too and that we must put aside pride

and work together, lest 'divided we fall' -under the weight of crushing and enslaving debt.)

Furthermore, in the absence of fundamental consumer protections (truth in lending; bankruptcy proceedings; statutes of limits; the right to refinance; adherence to usury laws; and,

Fair Debt & Collection practices, etc.), the government and lenders (banks) make more money in interest and particularly, in fees, if the student defaults on the loan, so there is a greater financial

incentive/motive for the government & banks to NOT help the student avoid default.

Therefore, seeing the crisis as outlined in this research paper, I would call upon Federal Lawmakers to pass legislation to:

**-A-** Prevent any more tax dollars[Figure-2] from going to Higher-Ed (be they grants(*) or loans –State or

Federal tax dollars) (*) NOTE: Gordon Wayne Watts, the author of this Position Paper, has reconsidered his view of elimination of grant

monies, funded by taxpayer dollars, and now would support *limited* grant monies to offset the very large loss if Federal Law prohibited the

government from making or guaranteeing loans. Liberals are partly right on this point: The money to run institutions of Higher Education must

come from somewhere. However, the use of *any* grant monies must be conditioned upon the frugal use of said tax dollars, which, in plain

English, to conservatives like Mr. Watts, means that these institutions can not use monopoly-style collusion and, in the case of State

Colleges, can not impose an excessive tax (tuition is a form of tax, as it flows to an arm of the government, State Colleges), *and* must

exercise personal responsibility and must neither spend lavishly, nor succumb to the pressures to distort the market, by charging an

artificially inflated high tuition, should grant and/or loan monies become available. Only then, if responsible spending practices were

adhered to would Mr. Watts be OK with use of taxpayer-funded grants to replace or offset losses if and when loans are discontinued or sharply

curtailed.

-- As in housing, this influx has distorted the

market, resulting in higher tuition. Taxpayers get raped twice by bailing-out[Figure-3] Higher-Ed:

*-1-* Once because it inflates tuition by enabling colleges’ 'addiction' to tax-dollars.

*-2-* Secondly, this 'addiction' is enabled by your tax dollars[Figure-2] -it costs you.

**-B-** Grant immediate forgiveness[14,28,36] to all unpaid student loans -and reset the debt to require students to owe only the free-market value of their education[Figure-1] (or, up to perhaps twice the

Free Market value –but no more), not the exorbitant prices[36] they were price-gouged through the monopoly-style collusion of the institutions of Higher-Ed & lenders/banks with the Federal Government.

**-C-** Although government regulation of tuition (e.g., a "Tuition Freeze") would normally be "Big Government Interference," and thus liberal, there is precedent that "Utility Ratemaking" would be

appropriate to control (by regulation) the costs of tuition, as is done with other industries classified as public utilities. Higher Education, legally, and by the definition, constitutes a public utility

since such businesses constitute a de facto monopoly for the services they provide within a particular jurisdiction. Since a monopoly exists when a specific person or enterprise is the only supplier of a

particular commodity, it can be argued that colleges are an enterprise, or group of businesses that have sole access to a market of higher education, as they are the only supplier of a college degree,

and are thus comparable to the monopoly of a group electric companies, who are the sole supplier of electricity, and thus subject to government regulation of rates. While this approach is used

successfully in many other industries where a monopoly would otherwise threaten the consumer, it is "liberal," and can not work in isolation, and thus, the other solutions outlined in this essay must also

be employed in order to save the quickly-sinking Higher Education industry in The United States.

**-D-** Other countries, such as Germany, have colleges that charge a student based on what they earn after they graduate, either via a voluntary contractual agreement known as a 'Tuition Contract' or by

involuntary regulation of fees by the government.[40] This method offers an incentive to colleges and universities, to provide a quality education, sufficient to enable their students to get

a decent job.

**-E-** [{(SAVING THE BEST FOR LAST)}] However, since most Lawmakers are cowards, and don't have the 'guts' to do A, B, C, or D, then here's an alternative: Return that standard consumer protections

to Student Loans (truth in lending; bankruptcy proceedings; statutes of limits; the right to refinance; adherence to usury laws; and, Fair Debt & Collection practices, etc.) -that were recently

removed.[12-14] WHY? Because, if Colleges/Universities knew that students could declare bankruptcy, they'd be more apt to charge a fair, free-market value for their product -instead of continued

indentured servitude slavery debt[26-27,38] for life -and, of course, this would afford life-saving relief to ALL students, past, present, and future –and set free a whole new generation of

slaves: Debt Slaves.[26-27,38]

If these five requirements were made Federal Law[34], then institutions of Higher-Ed, like Wal-Marts, MacDonald's, and K-Marts, could experience the free market pressures to offer a

higher quality -not a propped up house of cards -which has been the source of the problems thus far. (And, yes: Just like the 'Housing' bubble burst, the 'Education' and 'Healthcare' bubbles will

burst too if major changes are not made -and the economy *will* crash.) These universities & banks know students must go to college to even have a 'chance' at a job in this economy, so big banks

& liberal colleges have a 'captive audience': Their targeting of students is like 'shooting fish in a barrel': These students don't stand a chance when tuition rates are obscenely

exorbitant. Students are told from their youth[35] that they need an education to compete in today's world; let’s not punish them for doing what is right.

However, any Congressman/Congresswoman or Senator unwilling to pass these basic consumer protections for Student Loans is suspect for influence from huge campaign contributions by banks

and bankers, unwilling to give up the 'mobster-like' protection from a student's ability to declare bankruptcy. Just remember one thing: "Follow the money."

Gordon Wayne Watts received a Bachelor’s degree from The Florida State University with a double major in Biological and Chemical Sciences with honors and was the valedictorian from

United Electronics Institute. Watts, a non-lawyer, is best known for his lawsuit on behalf of Terri Schiavo[29], which lost 4-3 in the Florida Supreme Court, arguably doing better than even then Governor

Jeb Bush’s similar suit[30] (lost: 7-0) or Terri Schiavo’s own family’s federal case[31] (lost: 2-1). Mr. Watts, who ran unsuccessfully for Dist. 64 Fla. House of Representatives[32], is a part-time

political activist while he searches for a full-time job in his field.

New:

ALL known LAW School abuse blogs

* AttorneyToTemp.Blogspot.com (Story of a former practicing attorney who regrets

giving so many years of life to the legal profession, and so many hard-earned dollars to repay law school debt, along with some tips for finding

non-legal work, and for repaying your student loans.)

* BitterLawyer.com

* ButIDidEverythingRightOrSoIThought.Blogspot.com (Blog of a

disenchanted lawyer.)

* ClassBias.Blogspot.com (This blog is devoted to discussion of class bias in higher

education. My specific interest is in legal education where most law professors are supplied by a small number of elite schools. I am interested in

the manifestations of this bias and solutions. My experience is that the bias affects everything from hiring to acceptable forms of dress and

discourse. The dominant characteristic of those in power is a “sense of entitlement.”)

* DupedNonTraditional.Blogspot.com (Super-Duper: The Non-traditional Law Student

Confidence Game)

* EsqNever.Blogspot.com (Sharing a quest to find a successful career in another field while

also trying to expose the law school scam.)

* FirstTierToilet.Blogspot.com (Just Another Blog by an Indignant Graduate for

Indignant Graduates. Includes the "Law School Scam Blog Roll.")

* FlusterCucked.Blogspot.com (Insights, snide comments, and news about the value of

higher education, the perils of going to law school, and America's race to the bottom.)

* ForgottenAttorney.Wordpress.com (A voice among the silent majority of

young attorneys.)

* InsideTheLawSchoolScam.Blogspot.com

* LawSchoolTuitionBubble.Wordpress.com (Research & commentary on the

Law School Tuition Bubble.)

* LifesMockery.Wordpress.com (Author is a “law school victim.”)

* OutsideLiesMagic.Blogspot.com (Law School Graduate who finds himself marginally

attached and awash in a sea of overeducated but underpaid, indentured peers who feel, and were, duped by the promise of a better life through debt

and the modern chemistry of The Law School Industrial Complex, a scam that has destroyed a generation out of greed.)

* PoetryForPants.Blogspot.com (Tales of a Fourth-Tier Nothing: A blog on the

legal profession.)

* PresTTTigious.Blogspot.com (The PresTTTigious Legal "Profession": A blog about

the country's most miserable "profession," law. – About Me: PresTTTige – “There aren't many degrees literally worth less than the paper they're

printed on. My J.D. is one.”)

* RoseColoredGlassesJD.Blogspot.com (Rose, Esq.: Spreading the anti-lawschool

gospel.)

* SubPrimeJD.Blogspot.com (A blog dedicated to exposing the law school & higher education

scam, the 'Ponzi-like' structure of the US economy and in opposition to the US war machine.)

* TemporaryAttorney.Blogspot.com (With over 5,000 daily visitors, help expose the

nasty sweatshops, swindling law schools, and opportunistic staffing agencies.)

* ThirdTierReality.Blogspot.com (Blog's goal is to inform potential law school

students & applicants of the ugly realities of attending law school.)

_ _ It bears repeating...

**_Read_this_first:__________

ALL known Active Petitions Websites

* Causes.com: (Education)

* Change.org: (search on 'tuition')

* SignOn.org: (Input 'tuition' and click the search icon)

*

WhiteHouse.gov: (click 'Filter by Issue' and select 'Education' and then click 'Filter Petitions')

ALL known INFO websites

* http://CenterForCollegeAffordability.org (Founded in 2006, The Center for

College Affordability and Productivity (CCAP) is an independent, not-for-profit research center based in Washington, DC. The CCAP exists to help

facilitate a broader dialogue on the issues and problems facing the institutes of higher education in the United States. Currently, their research agenda

includes the following areas: Student Financial Aid Policy; Rising Costs of College; Causes of Higher Education Inefficiencies; Productivity of Staff

and Faculty Members; For-Profit Higher Education; and, Accreditation Old

Blog: CollegeAffordability.Blogspot.com)

* ConsumerFinance.gov (Know Before You

Owe: Student Loans

* Ed.gov (U.S. Dept. of Education)

* EduBubble.com/dpp (A redirect

from: EduBubble.com) A site about the book: Beating the College Bubble, which provides both a

free down-loadable version as well as a print version for a fee.

* EducationNews.org

* EducationSector.org

* FastWeb.com

* FinAid.org

*

FrugalDad.com (COLLEGE ISN’T CHEAP - with graphic)

* (Provided to The Register by Kimberly Hayes and archived below in case link above goes down)

* COLLEGE ISN’T CHEAP - graphic: Mirror 1Mirror 2Mirror 3

* Kimberly's grant of permission -and covered by both Fair Use & Creative Common's license: Mirror 1Mirror 2Mirror 3

Since publication of this research paper, I have spoken with my congressman, U.S. Rep. Dennis A. Ross (R-Fla.-12), and the outcome has been nothing less than incredible. First, I sent him

an email[37], to which he responded. I tried to email him through AOL, but he deleted my email

[link: copy a or

copy b] probably because it had an email attachment --and he was being careful to avoid a computer

virus. However, notice that link: When I resent my email, this time without any attachment [link: copy

a or copy b], he still deleted it too. Huh? So, when I found out new information on the

legislation, I emailed him through Facebook again[37]. If you will notice, in his reply, Rep. Ross claimed that: "Allowing discharge in bankruptcy for student loans would cause a sharp decline in

availability of loans," however this is patently false: As this expert has said

((cache: link 'a') or

(cache: link 'b')), "This report demonstrates only a slight increase in the availability of

private student loans to borrowers with low credit scores after BAPCPA made such loans non-dischargeable [in bankruptcy proceedings]," so, if consumer protections (like truth in lending; bankruptcy

proceedings; statutes of limits; the right to refinance; adherence to usury laws; and, Fair Debt & Collection practices, etc.) were restored to Student Loans, then there would probably only be a slight

*decrease* in the availability of private student loans --those not made or guaranteed by the Federal Government (since banks would be unwilling to lend to a small number of people who could not

afford to pay back --but that would be a good thing: They don't need to be borrowing anyhow). --Source: Student Aid Policy Analysis:Impact of the Bankruptcy Exception for Private Student

Loans on Private Student Loan Availability, by: Mark Kantrowitz, Publisher, FinAid.org, August 14, 2007 -- Furthermore, as I had pointed out in my last reply to Congressman Dennis Ross, credit

card loans are typically on the same terms (interest, payment options, fees, etc.) as these private loans, and yet credit card loans have continued unabated -and that even someone with bad credit can find

a lender. Besides 'private' loans, due to the recent changes in law, the Federal Government also now lends directly to students for Student Loans, so no 'sharp decline' in loans would result; furthermore,

the Congressman was wrong to oppose H.R. 5043 on these grounds, as it only returned standard consumer protections to private, not federal, loans. Lastly, as I pointed out (and the Congressman has NOT

rebutted or answered me on this point), it would probably be a *good* thing for there to be a "sharp decline" in Student Loans: This is the way it was in the 1950's, where there was little or no

loans, grants, or other 'student aid' for college education: Colleges knew they could not over-charge students, and college administrators learned to live within their means --and, guess what: American

colleges were the best in the world, so they did not need to overcharge students like they are doing today.

Besides being factually wrong on a number of points, the Congressman engaged in a bit of bizarre behaviour: Besides deleting my email without reading it --twice

[link: copy a or

copy b], and blocking me from his Facebook for no apparent reason

[link: copy a or

copy b], he was rather rude and repeatedly evaded answering a question that two (2) of his constituents

posed to him: [link: copy a or

copy b] on his 'Politician' page.

In all fairness to the Congressman, he only blocked me from his personal Facebook page, not his 'Politician' one; nonetheless, he seems to discuss politics with his constituents much

less on his politician page, and as I've done nothing to provoke or insult him (other than express my views, and politely ask for representation), his reactions and odd behaviour are unwarranted --and

actually a bit bizarre. -- It makes me think that he is being paid off by big banks who want protection from the Free Market pressures of failure (aka a 'bailout' from having borrowers be able to

file bankruptcy) that would result if the standard consumer protections for Student Loans (truth in lending; bankruptcy proceedings; statutes of limits; the right to refinance; adherence to usury laws;

and, Fair Debt & Collection practices, etc.) were returned to Student Loans --as the law was in the past. -- Since all other loans have standard consumer protections, young, vulnerable college students

should not be deprived either. This is doubly true now that college tuition is skyrocketing to obscenely high levels --even as a quality of education continues to plummet -and other nations continue to

outperform us in math and the sciences. So, we see that this influx of Federal 'student aid' has actually made things worse. Why then do supposedly 'conservative' Congressman like Rep. Ross, continue to

interject Big Government into Higher Education when: (-a-) it goes against their 'Smaller Government' mantra; and, (-b-) It has been proven to NOT work?

(Friday, 01 July 2011)UPDATE:

To his credit, Rep. Dennis A. Ross (R-Fla.12), has addressed a few of the complaints of banning people from his 'Politician' page

[link: copy a or

copy b], but, as yet, has refused to address MANY other concerns, and one

reply that he eventually made was just a little bit weird: [link: copy a or

copy b] --still, a bit bizarre, if you ask me: He is our elected

representative. Lastly, since he's not only removed me from his regular Facebook (http://Facebook.com/RepDennisRoss), but also

BLOCKED me from even seeing his Facebook Wall: [link: copy a or

copy b] --and were it not for a good friend letting me look at his Facebook

[link: copy a or

copy b], I would not even have seen the Public Education post.

I bet Rep. Ross was not expecting this, but I 're-posted' his link from his personal Facebook to his 'Politician' Facebook fan page.

If college student suicides due to Student Loan defaults has seen a dramatic rise[15-18;36], as I've previously documented, then this problem is real, not just a financial problem

'on paper': I hope my Congressman starts caring about his constituents & voters and responding by both replying AND introducing bills that will solve these problems, but as yet, his behaviour is a

bit unresponsive and on occasion a bit bizarre.

"Insanity" is doing the same thing (socialist government involvement into higher-ed, & removal of Free-Market checks, like standard consumer protections

on Student Loans), and expecting a different result. Either our Representatives & Senators are 'insane' --or being bought off by Big Banks --or both?

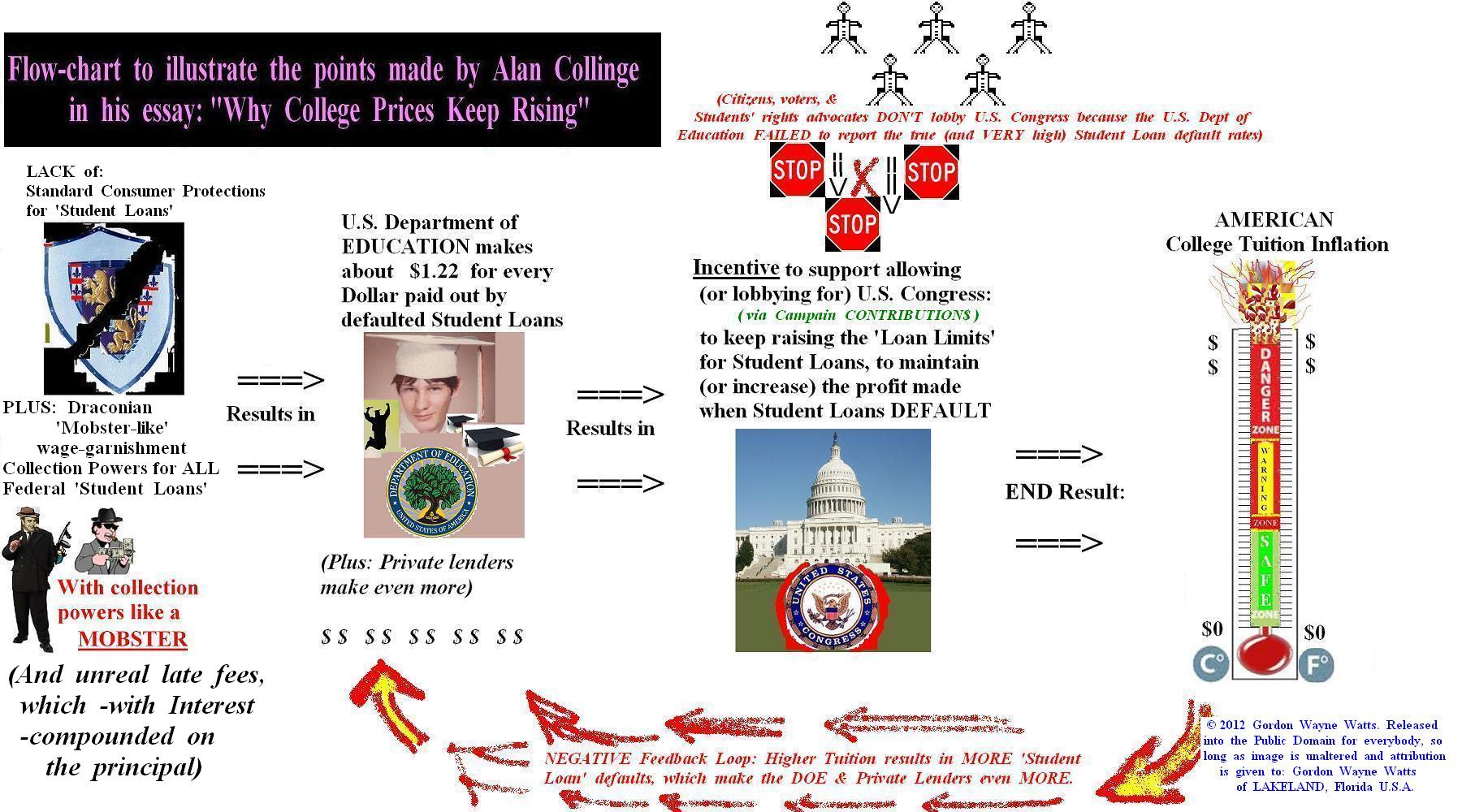

For many years, it has been unknown to the general public that all of the major

elements comprising the student lending system (i.e. lenders, collection companies, guarantors) made far more money when

students defaulted on their loans. Nevertheless, this is a fact, and it is well documented. It is most disturbing,

however, that recent analysis of the President’s Budget data reveals that even the US Department of Education, on

average, recovers $1.22 for every dollar paid out in default claims. Assuming generous collection costs, and even

allowing for a nominal time value of money of a few percent (the governments cost of money is very low), it still appears

that the federal government, even, is making a pretty penny from defaults.

How could this be possible? The primary reason for this is that unlike all other types of debt, bankruptcy

protections, statutes of limitations, and other standard consumer protections have been removed from federal student

loans, and draconian collection powers have been given to collect on hugely inflated, defaulted student loan debt.

The systemic consequences of these types of financial motivations are too numerous to describe here, but one very

significant result is that during the legislative process, when the schools, lenders, and their lobbyists pressure

Congress to raise the allowable loan limits, the Department of Education-one of the only entities available to act

in the interest of the students and call for a freezing (or even a reduction in the lending limits)- has repeatedly

failed to tell it like it is regarding defaults. The schools and lenders point and brag about the low “cohort” default

rates, but this metric (which hit a low of about 4% in 2005) masks the true default rate, which we now know was likely

25% or higher for years, and today is likely significantly higher than that.

Instead of voicing concern, or even objections to Congress in the lending limit debates, the Department of Education

remained largely silent, despite their knowledge about the true default rate for years, and in fact, press releases

about the default rate spanning years from the Department of Education speak exclusively of the cohort rate, and this

continues to this day, by and large, although media have shed some light on the true default rate in recent years.

This, again, is a key failure in oversight that effectively causes Congress to make decisions without the interests of the

borrowers being represented (Of course the lenders and schools claim to have the interests of the students at heart,

but their obvious financial motivations discount their credibility on this claim). Therefore, Congress continues

to rubber-stamp these legislative efforts, and the schools quickly raise their tuition to bump up against the new

lending ceilings.

If the Department of Education were seeing a material, financial loss with loan defaults, they likely would be far more

assertive about the reasons NOT to raise the loan limits…and this would provide a critical check on the process.

But the Department has been largely absent from these debates, and its misaligned interest is certainly the reason why.

So it must be agreed that lack of Department oversight contributes directly to repeated votes by Congress to raise the

loan limits, and we’ve already established the link between this poor oversight, and the removal of consumer protections.

So undoubtedly, the removal of standard consumer protections has effectively allowed the schools and lenders to have

their way with Congress on this issue.

Critics could argue that the established student advocacy groups should have stepped in to fill this role…and this is

obviously true…but the advocates can claim that they did not know that defaults were as high as they were (recent evidence

suggests that the true default rate exceeds 1 in 3), therefore any objections from them (assuming they did object) were

not strong. Had they known that defaults were as high as they were, one can only assume that they would have objected

far more forcefully, starting many years ago.

The current debate surrounding the cause of tuition inflation is a confusing mix of rhetoric that typically involves

fingers pointing in all directions…”like a scarecrow in the wind” …among lenders, schools, the Department of Education,

the student advocates, and Congress. But of these five entities, four were behaving as expected (i.e. schools pushing

for raising the limits, advocates wringing their hands in the absence of defensible proof that things were going awry,

lenders playing their part as the selfish, amoral entities they are understood to be, Congress debating what they are

told, and ultimately voting based upon this debate).

The Department of Education, however, failed to fulfill its role, and did not disclose to the group the true magnitude of

the default problem, as one would expect it to. Therefore the Department is clearly the party whose behavior can

ultimately be questioned with strong justification. Of course citizens have every right to be seethingly resentful and

angered by all of these actors failing to point out what was obvious…that the students were being saddled with outrageous

increases in student loan debt (I believe the advocates bear a tremendous amount of responsibility, for example), but

strictly speaking, the Department’s failure is the only one with zero defense.

This is a critical, unambiguous link that is never pointed out, but which is key- the key- to explaining the rampant

inflation we have seen in academia over the years. Congress and the president should be demanding to know why key

personnel at the Department so badly neglected to fulfill their duties, and take a hard, hard look at the corporate

culture that has enabled this sort of gross neglect of basic functions. And of course, the standard consumer protections

that should have never been removed from student loans must be returned at the earliest possible opportunity.

_______ Editor's Note: Mr. Collinge makes some very strong claims above, such as regarding the amount of

profit that the U.S. Department of Education makes on defaulted loans, but The Register has carefully researched

his claims, and –so far as we can see –they are correct and can easily be documented by a routine web search on the subject.

His op-ed originally appeared

here on Forbes.com, on 03/19/2012, as a guest post in Peter J. Reilly's regular column, which focused on the tax issues

of individuals, businesses, as well as related financial matters. Mr. Collinge was good enough to authorise

The Register to re-publish and archive his fundamentally important analysis here, so long as it was unaltered and

re-printed in its entirety -with no additions, subtractions, or alterations to the piece (other than, of course, style and

formatting issues), and The Register felt that it would be a good precaution to archive this piece on multiple

websites, not "putting all our eggs in one basket," since it is not a widely known fact that the lack of bankruptcy

protections for Student Loans was a major factor in the meteoric 'tuition inflation' in recent decades, in spite of

declining quality of America's standings in Higher Ed rankings in STEM (Science, Technology, Engeneering, & Math). Mr.

Collinge is the founder of

StudentLoanJustice.org, a Political Action Committee dedicated

to the mission of changing unjust laws related to how student loans are handled. He is also the author of the

ground-breaking exposé,

"THE STUDENT LOAN SCAM: The Most Oppressive

Debt in U.S. History–and How We Can Fight Back,", available at all major book sellers, and available in both

paperback (ISBN-13: 978-0-8070-4231-1) and hardback (ISBN-13: 978-0-8070-4229-8)

versions, such as the

[Paperback] version on AMAZON (here)

or

[Hardcover] version on AMAZON (here), or even

the KINDLE version (here).

If Donald Trump (rich and conservative), Solyndra (rich and liberal), and ALL rich-&-powerful Wall-Street bankers can file for

bankruptcy (and they don't even need it: they are rich), why not students? Read this -- re-read this -- and follow the links above.-Editor

Sources:

[1] "Massive increases in higher-ed costs a mystery to be solved," Virgil Swing (DuluthNewsTribune.com), May 15, 2008,

(http://www.duluthnewstribune.com/event/search of: "Virgil Swing: Massive increases in higher-ed costs"),

**

http://www.google.com/search?hl=en&q=%22Budgeteer+News%22+%22Virgil+Swing%22+2008+may+15&start=20&sa=N&filter=0,

**

http://search.yahoo.com/search;_ylt=A0geu5Vnxr9KXSsBZFJXNyoA?p=%22Budgeteer+News%22+%22Virgil+Swing%22+2008+may+15&fr2=sb-top&fr=yfp-t-501&sao=0,

** http://gordonwaynewatts.com/FannyDeregulation/VirgilSwingArticle.JPG,

** http://gordonwatts.com/FannyDeregulation/VirgilSwingArticle.JPG

[2] "Student Aid and College Tuition: The Upward Spiral," by David W. Kirkpatrick, Nov 01, 2007

http://www.schoolreport.com/schoolreport/articles/College_Tuition_11_07.htm states: "In my personal case, while a student at a public

college in the 1950s, tuition was $100 per semester. There was no aid but neither was there any debt at graduation."

[3] "2008 inflation rate at 0.1%, slowest gain in 54 years for consumer prices"

http://www.usinflationcalculator.com/inflation-rates/2008-inflation-rate-at-01-slowest-gain-in-54-years-for-consumer-prices/1000357

[4] "Average college cost breaks $30,000: Average for 4-year private school passes key mark; total costs for both public and private schools up well above inflation,"

Rob Kelley, Oct 27 2006,

http://money.cnn.com/2006/10/24/pf/college/college_costs/index.htm states: "The average tuition at four-year public colleges and universities is $5,836 for the

2006-07 school year…With room and board, four-year public colleges average $12,796 for in-state residents." The $5,836 figure for tuition would be either $6,227.39 or $6,057.77 in 2008,

according to the WestEgg inflation calculator, depending on whether you use 2006 or 2007 as your initial year. The average of those two figures is $6,142.58 for college tuition in 2008

[5] "Preparing to Go to College," p4,

http://www.pearsonhighered.com/assets/hip/us/hip_us_pearsonhighered/samplechapter/0131716662.pdf states: "According to The College Board, the average college housing costs in the

2004–2005 academic year were about $6,222," which would be either $7,036.63 or $6,805.25 in 2008, according to the WestEgg inflation calculator, depending on whether you use 2004 or 2005

as your initial year. The average of those two figures is $6,920.94 for college housing in 2008

[6] Adding $6,920.94 for housing & $6,142.58 for tuition yields $13,063.52

[7] http://www.westegg.com/inflation conversion: "What cost $138 in 1956 would cost $1081.50 in 2008," & "What cost $138 in

1957 would cost $1043.92 in 2008," whose average is $1,062.71

[8] “Criminally insane, but out on the street” (By NICHOLAS K. GERANIOS (AP) – Oct 17, 2009 - SPOKANE, Wash. (AP) -- “Phillip A. Paul in 1987 was declared criminally insane for killing

an elderly woman after voices in his head told him she was a witch…He obtained several credit cards and went on shopping sprees that led to a bankruptcy filing.”

http://hosted.ap.org/dynamic/stories/U/US_CRIMINALLY_INSANE?SITE=RIPRJ&SECTION=HOME&TEMPLATE=DEFAULT ~

http://www.google.com/hostednews/ap/article/ALeqM5gH6QbyQfjoqwCFxHJpNb067G_96gD9BD0N5O0 ~

http://www.msnbc.msn.com/id/33358068/ns/us_news-crime_and_courts ~

http://www.kansascity.com/news/nation/story/1514284.htmlhttp://news.yahoo.com/s/ap/20091017/ap_on_re_us/us_criminally_insane/print

[9] “25 Rich Athletes Who Went Broke” (BusinessPundit.com, May 18, 2009) “Scott Harrison…The pride of Scotland had problems with drinking, drugs and consequently the law. A world champion

in 2003, Harrison’s life later spun out of control. In 2006, he pulled out of a fight to check into rehab. By July 2007, the ever-classy Harrison declared bankruptcy after losing his last

fight…over unpaid taxes.” http://www.businesspundit.com/25-rich-athletes-who-went-broke

[10] “STATEMENT OF THE NATIONAL MULTI HOUSING COUNCIL, et al.,” (BEFORE THE U.S. HOUSE COMMITTEE ON JUDICIARY, MARCH 3, 2003) “A resident who was being evicted for selling drugs on the property

declared bankruptcy.” http://www.nmhc.org/Content/ServeFile.cfm?FileID=3511

[11] “Bankrupt: Maxed Out In America” (American RadioWorks, public radio, Saturday, April 22, 2006) “Over the past decade, 15 million people declared bankruptcy. That's better than double the

figure from the previous decade.” (No doubt, many criminally insane and/or drug users were among them, but students, trying to better themselves, are not permitted to file for bankruptcy when

they get overwhelmed by debt, penalties, and compounding interest. See also, note: "36" below regarding the Bible standards on interest fees charges for loans.)

http://americanradioworks.publicradio.org/features/bankruptcy/transcript.html ~

http://www.accessmylibrary.com/article-1G1-144728950/radio-documentary-focus-bankruptcy.html

[12] “Student Loans & Bankruptcy” (Student Loan Borrower Assistance Project, a program of the National Consumer Law Center) “Student loans are not usually discharged in bankruptcy. It is

difficult, but not impossible, to do so if you can show that payment of the debt “will impose an undue hardship on you and your dependents.”

http://www.studentloanborrowerassistance.org/bankruptcy

[13] “Student Loans In Bankruptcy” (Lawyers.com) “Student loans are not dischargeable in bankruptcy unless you can show that your loan payment imposes an "undue hardship" on you, your family,

and your dependents. Non-dischargeable debts are those debts that you cannot totally eliminate when you file for bankruptcy and will have to be paid by you. It is almost impossible to show

an undue hardship unless you are physically unable to work and the chances of your obtaining any type of gainful employment in the future are non-existent.”

http://bankruptcy.lawyers.com/Student-Loans-In-Bankruptcy.html

[14] “Student Loan Bankruptcy Options” (MoneyZine.com)

“In the normal course of bankruptcy, student loans will not be discharged or forgiven. However, after the proceedings are over, an adversary proceeding can take place

in bankruptcy court to decide if you meet all three of the hardship rules or tests. In this adversary proceeding, the student loan creditors will be present to challenge

your hardship request. You must be able to satisfy all three of the following tests in the eyes of the court:

•If you were forced to repay the student loan, then you will not be able to maintain a minimal standard of living.

•You are able to present evidence that this financial hardship will continue for a significant period of time over the remaining term of the student loan.

•A good faith effort was made to repay your student loan before you filed for bankruptcy. Effectively this means you have been faithfully repaying your college loan

for a minimum of five years.

If your loan is discharged, you will not have to repay the remainder of the money owed these creditors. However, you may have trouble getting a student loan of any kind in the future.”

http://www.money-zine.com/Financial-Planning/College-Loan/Student-Loan-Bankruptcy-Options See

also: http://ForgiveStudentLoanDebt.com

[15] “Crushing debt” (Chicago Sun-Times, BY DAVE NEWBART) September 24, 2007 "Jan Yoder was preparing for her son's funeral when the phone rang. It was another student loan collector wanting to

know when her son would pay up…It was those calls and the burden of crushing debt, she says, that led her depressed son to take the drastic action of killing himself late

last month. ''When it gets to the point where people are fleeing the country, going off the grid or taking their own lives, you know something has gone horribly wrong,'' said Alan Collinge,

founder of Student Loan Justice, which is pushing to change student lending laws.”

http://www.ibhe.state.il.us/NewsDigest/NewsWeekly/092807.pdf (Higher Ed NewsWeekly: from the Illinois

Board of Higher Education, page 57) ~

http://nalert.blogspot.com/2007/09/student-loan-debt-drives-man-to-suicide.html (Newsalert) See also: http://StudentLoanJustice.org

[16] “I’m Thinking of Suicide Because of My Student Loans. – John” (GetOutOfDebt.org, undated news story) “Dear Steve, My student loans are almost $42,000 dollars. I pay almost $260 dollars

per month and all but $12 dollars is interest and the principal continues to go higher…I frequently think about suicide; thinking about my son is the only thing that has so far kept me

from committing suicide. John”

http://getoutofdebt.org/5493/im-thinking-of-suicide-because-of-my-student-loans-john See also, note: "36" below regarding the Bible standards on interest fees charges for loans.

[17] "A Pastor's Student Loan Debt" (NPR, by Libby Lewis) July 14, 2007 “Dan Lozer's tiny paycheck means he'll be paying off those loans until 2029...Lozer said there was a time when he thought

about suicide.” http://www.npr.org/templates/story/story.php?storyId=11980696

[18] “Company’s march toward student loan monopoly scary” (The News Tribune, By ALAN COLLINGE) 06/19/07 “In Boston; a medical student can’t get licensed because he can’t pay $52,000 on what began

as a $3,000 debt. A suicide in Oregon. A suicide in Maryland. People who have fled the country due to the explosion of their student loan debt. The list goes on and on.”

http://www.thenewstribune.com/opinion/othervoices/story/90638.html See

also: http://StudentLoanJustice.org

[19] "U.S. Teens Trail Peers Around World on Math-Science Test," Maria Glod, Washington Post, Dec 5, 2007; Page A07

http://www.washingtonpost.com/wp-dyn/content/article/2007/12/04/AR2007120400730.html

[20] "U.S. falls in education rank compared to other countries," Elaine Wu (U-Wire), 10-04-2005, The Kapi‘o Newspress

http://www.google.com/search?hl=en&q=%22falls+in+education+rank+compared+to+other+countries%22+%22Elaine+Wu%22&aq=f&oq=&aqi= And

http://search.yahoo.com/search?p=%22falls+in+education+rank+compared+to+other+countries%22+%22Elaine+Wu%22&toggle=1&cop=mss&ei=UTF-8&fr=yfp-t-832

(Key phrases search: "falls in education rank compared to other countries" "Elaine Wu")

[21] "U.S. slips lower in coding contest: In what could be an ominous sign for the U.S. tech industry, American universities slipped lower in an international programming contest," Ed Frauenheim,

News.com, Posted on ZDNet News: Apr 7, 2005 http://news.zdnet.com/2100-9595_22-142206.html

[22] Sean Hannity, from 7:22-8:22, concurs with this analysis -and with me: We’ve been "dumbed down" and our public schools are "mediocre at best." At 8:22+, he says "taxpayers ought not foot

the bill" for Higher-Ed. From 4:59-5:13, he makes the ‘6am to midnight’ comments.

http://www.youtube.com/watch?v=m3ogGD17pq4&feature=channel_page ** Cached:

http://www.GordonWayneWatts.com/FannyDeregulation/21-22Sept2009-Hannity-Call-In.mp3

and http://www.GordonWatts.com/FannyDeregulation/21-22Sept2009-Hannity-Call-In.mp3.

Newly added comment:I don't mean any offense or disrespect to Sean Hannity, but I must now update my research paper here to clarify and point out one glaring FACT: Mr. Sean Hannity is a

hypocrite -While he has no problem with student's tuition (a form of tax: see above) being jacked up almost one-thousand (1,000%) percent, LOL, nonetheless, I am quite sure that he could cringe

at the discovery that *his* income taxes increased by the same amount. IN HIS DEFENSE, I realise that he would probably say that this is not an equal comparison -ah, but is it?? --Well, he has

no choice but to get a job of some sort to make money, and, likewise, the students nowadays, have no choice but to get an education if we are to compete in the global market. So, the comparison

is indeed equal. I say all this to underscore the double-standards and hypocrisy the rich have for those similarly-situated who are poor -even the "conservative" rich, like Hannity. THAT is the

reason our country is falling: Lack of care for our neighbour. That all needs to change -and it will upon arrival of Jesus. In time.--END OF COMMENT

[23] As odd as this sounds -that a meal will be 100 or 200 dollars many religious conservatives do believe this will happen in the very near future -due to end-times prophecies such as this

one: "And I heard a voice in the midst of the four beasts say, A measure of wheat for a penny, and three measures of barley for a penny; and see thou hurt not the oil and the wine." (Holy Bible,

Rev 6:6 KJV) "…[The price: It will be a] quart of wheat [a day’s worth of human food] for a denarius [a whole day's wages], and three quarts of barley [daily measure of food used for

livestock also sold] for a denarius…" (Holy Bible, Rev 6:6 AMP) Cf II Kings 6:25, another similar occasion. (Some comments in bracket not in original but added for clarity)

[24] In 1st Samuel 22:1-2, people were probably over-taxed and in debt, and without a doubt this was the case with Solomon’s not-so-wise son, Rehoboam, as told in 1st Kings 12:1-16

-almost all of his citizens revolted and kicked him out as king for his stated plans to over-tax his constituents.

[25] "And whosoever shall compel thee to go a mile, go with him twain." (Holy Bible, Matt 5:41 KJV)

[26] In Dred Scott, a 7-2 majority of America's highest court, not too long ago, held that "[T]he negro might justly and lawfully be reduced to slavery for his benefit." Chief

Justice Roger B. Taney, writing for the Court. Dred Scott v. John F. Sanford, 15 L.Ed. 691; 19 How. 393; 60 US 393 at 407.(US 1857).

[27] Key Phrase search:

http://www.google.com/search?hl=en&source=hp&q=%22debt+slaves%22&aq=f&oq=&aqi=g1g-m1 and

http://search.yahoo.com/search?p=%22debt+slaves%22&fr=yfp-t-501&toggle=1&cop=mss&ei=UTF-8

[28] This is not the first time in history blanket forgiveness of debts has been considered: “1At the end of every seven years you shall grant a release of debts. 2And this is

the form of the release: Every creditor who has lent anything to his neighbor shall release it; he shall not require it of his neighbor or his brother, because it is called

the LORD’s release…9Beware lest there be a wicked thought in your heart, saying, ‘The seventh year, the year of release, is at hand,’ and your eye be evil against your poor brother

and you give him nothing, and he cry out to the LORD against you, and it become sin among you. 10You shall surely give to him, and your heart should not be grieved when you give to him,

because for this thing the LORD your God will bless you in all your works and in all to which you put your hand. 11For the poor will never cease from the land; therefore I command you,

saying, ‘You shall open your hand wide to your brother, to your poor and your needy, in your land.’” (HOLY BIBLE, Deuteronomy 15:1-11, NKJV) Those 'moral conservatives' who would suggest this

is not fair for those students who have already repaid their debts should note that in the Deuteronomy passage above, no allowance is made for special treatment for those debtors who had repaid

their debts -they just had to 'tough it out' and be glad their neighbors' debts were forgiven. This is the kind of ‘tough love’ that is needed to address the higher education and bankruptcy

crisis hitting our nation, not unlike the ‘hard-line’ advice given in both Old and New Testaments regarding how to address housing and homeless issues. Isaiah 58:6-7 (Old Testament) demands

that you take in the homeless wandering stranger -and no less than Jesus, Himself, in the New Testament (Matthew 25:31-46) repeats this same demand -echoing all sustentative requirements

laid down by the prophet Isaiah: Jesus makes no bones about the consequences for not feeding the hungry, clothing the naked, or taking in the homeless: With Divine authority conferred upon Him,

Jesus does no less than send the malefactors directly to Hell. -- Jesus also said: "And whenever you stand praying, if you have anything against anyone, forgive him and let it drop

(leave it, let it go), in order that your Father Who is in heaven may also forgive you your [own] failings and shortcomings and let them drop." (Mark 11:25, Holy Bible, AMP) -- LASTLY, Jesus also

said: "...forgive, and ye shall be forgiven. (Luke 6:37b, Holy Bible, KJV) -

See also: http://ForgiveStudentLoanDebt.com

[29] In Re: GORDON WAYNE WATTS (as next friend of THERESA MARIE “TERRI” SCHIAVO), No. SC03-2420 (Fla. Feb.23, 2003), denied 4-3 on

rehearing. http://www.floridasupremecourt.org/clerk/dispositions/2005/2/03-2420reh.pdf

[30] In Re: JEB BUSH, GOVERNOR OF FLORIDA, ET AL. v. MICHAEL SCHIAVO, GUARDIAN: THERESA SCHIAVO, No. SC04-925 (Fla. Oct.21, 2004), denied 7-0 on

rehearing. http://www.floridasupremecourt.org/clerk/dispositions/2004/10/04-925reh.pdf

[31] Schiavo ex rel. Schindler v. Schiavo ex rel. Schiavo, 403 F.3d 1223, 2005 WL 648897 (11th Cir. Mar.23, 2005), denied 2-1 on

appeal. http://www.ca11.uscourts.gov/opinions/ops/200511628.pdf

[32] Key Phrase search:

http://www.google.com/search?hl=en&q=%22florida+house%22+64+%22gordon+wayne+watts%22&cts=1255495265724&aq=f&oq=&aqi= and

http://search.yahoo.com/search?p=%22florida+house%22+64+%22gordon+wayne+watts%22&fr=yfp-t-155&toggle=1&cop=mss&ei=UTF-8

[33] One example of wasteful spending I could not fit in due to word-length (this research paper is already exactly 1,575 words in the body only -not counting the title, references, or footer), was

the requirement for students to purchase the newest edition of textbooks every year. This is entirely untenable, since many sciences -such as Physics and Math -have not changed sustentatively

in the last century: The Laws of Physics aren’t just going to change all of a sudden -and the newer developments do not need new textbooks (such as one friend who reports that he paid $1,500.oo

for *each* of his children for new textbooks). The Higher-Ed textbook industry is a “Cash Cow,” milking students. One alternative is to have textbooks online -or -in portable “e-books.”

Another is to require only supplemental materials be purchased -or downloaded. However, no matter how you slice it, students are getting juked and played like a piano -and milked like a cow.

America’s good name is tarnished when education costs more -and does less -than other countries. I don’t wish to offend other countries (they beat us fair and square), but this game must not

continue: Just like in war, everybody loses when it played.

[34] My friend, Eddie Adams, Jr., who is a genuine conservative (one of many true conservatives this

election cycle) running for U.S. Congress in a neighboring district, was recently interviewed by me

for my newspaper's coverage (main link

- alt. link) of the Districts 11 and 12 House races. When I asked him about pouring tax dollars

into higher-ed, he responded predictably and as expected -he opposed such; however, when I asked him whether he supported standard bankruptcy protections for student loans as with

credit cards users, he said they should pay them back -as he did (invoking the personal responsibility motif). While I respect his work ethic and feel he has earned a right to his opinion,

I genuinely feel he was wrong on the merits (because I feel students should only pay back the value of their education -not the inflated amount they were forced to accept due to the collusion

of the institutions of higher-ed). Since he, like myself, is a Christian, who adheres to the Bible as infallible

scripture (his grandfather was a Baptist preacher), I was inspired to review the Lord's standards

on this topic, and I credit Eddie for so inspiring me. It is my belief that all true followers of Christ will be conformed to the renewing of the scriptures, and so I write this with the

hope that Eddie will slowly, but surely, change his viewpoint herewith: This section below is directed only at Bible-believing Christians -and, while trying to "win converts" is good,

that is not what this section is saying:

‘Practical’ considerations: What’s helpful for *you* 7 “Be not deceived; God is not mocked: for whatsoever a man soweth, that shall he also reap.” -Galatians 6:7 (KJV)

TRANSLATION: Karma has a biting way about it: What goes around comes around, so don’t jack the students out of their fair value by **greatly** overcharging them

for their education –simply because they're a captive audience -and a captive market.

‘Legal’ considerations: What’s helpful according to the *government* 1 “Let every soul be subject unto the higher powers. For there is no power but of God: the powers that be are ordained of God. 2 Whosoever therefore resisteth the power, resisteth the ordinance of God: and they that resist shall receive to themselves damnation. 3 For rulers are not a terror to good works, but to the evil. Wilt thou then not be afraid of the power? do that which is good, and thou shalt have praise of the

same:” -Romans 13:1-3 (KJV)

COMMENTARY: If monopoly or collusion laws were broken –and/or if excessive fines imposed upon student that are not even legal for credit card users (the latter implicating Equal Protection),

then this would be illegal –and, besides violating ‘Man’s Law,’ the rich leaders profiting off of students would also be in violation of this section of God’s standard.

‘Moral’ considerations: What’s helpful for *others* 12 “In everything, therefore, treat people the same way you want them to treat you, for this is the Law and the Prophets.” -Matthew 7:12 (NASB)

16b-17a “…Judge fairly between each person and his fellow or foreigner. Don't play favorites; treat the little and the big alike; listen carefully to each.

Don't be impressed by big names. This is God's judgment you're dealing with...” -Deuteronomy 1:16b-17a (The Message)

3 “Defend the poor and fatherless: do justice to the afflicted and needy.” -Psalm 82:3 (KJV)

21 “Though hand join in hand, the wicked shall not be unpunished: but the seed of the righteous shall be delivered.” -Proverbs 11:21 (KJV)

22 “Do not exploit the poor because they are poor and do not crush the needy in court, 23 for the LORD will take up their case and will plunder those who plunder them.” -Proverbs 22:22-23 (NIV)

8 “Speak up for those who cannot speak for themselves, for the rights of all who are destitute. 9 Speak up and judge fairly; defend the rights of the poor and needy.” -Proverbs 31:8-9 (NIV)

11 “When the sentence for a crime is not quickly carried out, the hearts of the people are filled with schemes to do wrong.” -Ecclesiastes 8:11 (NIV)

20 “Humility is an abomination to the proud; likewise the poor are an abomination to the rich. 21 When the rich person totters, he is supported by friends,

but when the humble falls, he is pushed away even by friends. 22 If the rich person slips, many come to the rescue; he speaks unseemly words, but they justify him. If the

humble person slips, they even criticize him; he talks sense, but is not given a hearing. 23 The rich person speaks and all are silent; they extol to the clouds what he says.

The poor person speaks and they say, "Who is this fellow?" And should he stumble, they even push him down.” -Sirach 13:20-23 (NRSV) Deuterocanonical Apocrypha

10 “If thou faint in the day of adversity, thy strength is small.” -Proverbs 24:10 (KJV)

28 “Strive for the truth unto death, and the Lord shall fight for thee.” -Sirach 4:28 (KJV)

28 “Fight to the death for truth, and the Lord God will fight for you.” -Sirach 4:28 (NRSV)

[35] In my Official Campaign pages (http://GordonWayneWatts.com/Campaign.html and

http://GordonWatts.com/Campaign.html), like most 'conservatives,' I had supported VOUCHERS for high schools and other public schools,

at least for 'equal treatment' of vouchers as with Pell Grants and Guaranteed Student Loans, but I was dead-wrong here:

Although I was right to support 'equal treatment' between vouchers (pre-K through high school) and Pell Grants & Guaranteed student loans (Higher Education, Universities, college),

I WAS WRONG to support vouchers AT ALL -for the same reason I was wrong to support and public funding of higher-ed: It distorts the market, feeding an addiction which results in higher tuition and

costs -all the while using tax dollars to feed this addiction. Thus, if I make a compelling case against liberals using tax dollars for higher ed (grants, loans), then the same problems must *logically*

exist with vouchers: Even though students and parents can make some choice in which high school to attend (some free market 'competition' forces are at work), the influx of tax dollars still distorts

the market (overall, that is), and the high schools realise they can raise tuition, since students can afford more. Thus, while intuitively against what we may feel, we must be consistent with our logic

and rationally conclude that the government should get OUT of education altogether: Both Higher Ed (colleges and Universities) as well as 'lower' ed: Pre-K through high school.

[36] Gordon's Story:

Long-story-short: My student loan is unfair "usury / interest" -prohibited by many Biblical scriptures enumerated below, and I am drowning in debt... (from the Amplified Bible)

-- This is the end of the "short" version. Below, this email is long, I warn the reader in all fairness. --

Matthew 25:27

Then you should have invested my money with the bankers, and at my coming I would have received what was my own with interest.

Luke 19:23

Then why did you not put my money in a bank, so that on my return, I might have collected it with interest?

Comment: Jesus does not say He agrees with interest being charged --He only acknowledges its existence; but, even assuming Jesus now approves of interest charged

on loans, a change from Old Testament times, nonetheless, He does *not* approve of over-bearing or oppressively crushing interest and charges, as described below -- You use Scripture to interpret

Scripture:

Exodus 22:25

If you lend money to any of My people with you who is poor, you shall not be to him as a creditor, neither shall you require interest from him.

Leviticus 25:36

Charge him no interest or [portion of] increase, but fear your God, so your brother may [continue to] live along with you.

Leviticus 25:37

You shall not give him your money at interest nor lend him food at a profit.

Deuteronomy 23:19

You shall not lend on interest to your brother--interest on money, on victuals, on anything that is lent for interest.

Deuteronomy 23:20

You may lend on interest to a foreigner, but to your brother you shall not lend on interest, that the Lord your God may bless you in all that you undertake in the land to which you go to possess it.

Nehemiah 5:7

I thought it over and then rebuked the nobles and officials. I told them, You are exacting interest from your own kinsmen. And I held a great assembly against them.

Nehemiah 5:10

I, my brethren, and my servants are lending them money and grain. Let us stop this forbidden interest!

Psalm 15:5

[He who] does not put out his money for interest [to one of his own people] and who will not take a bribe against the innocent. He who does these things shall never be moved.

Proverbs 28:8

He who by charging excessive interest and who by unjust efforts to get gain increases his material possession gathers it for him [to spend] who is kind and generous to the poor.

Ezekiel 18:8

Who does not charge interest or percentage of increase on what he lends [in compassion], who withholds his hand from iniquity, who executes true justice between man and man,

Ezekiel 18:13

And has charged interest or percentage of increase on what he has loaned [in supposed compassion]; shall he then live? He shall not live! He has done all these abominations; he shall surely die; his

blood shall be upon him.

Ezekiel 18:17

Who has withdrawn his hand from [oppressing] the poor, who has not received interest or increase [from the needy] but has executed My ordinances and has walked in My statutes; he shall not die for the

iniquity of his father; he shall surely live.

Ezekiel 22:12

In you they have accepted bribes to shed blood; you have taken [forbidden] interest and [percentage of] increase, and you have greedily gained from your neighbors by oppression and extortion and

have forgotten Me, says the Lord God.

The Details:

Right out of high school, I went to the local community college in my area under a “merit scholarship,” because of my grades (top 10% in high school), but, since I was a kid, I lost the

scholarship after 3 semesters due to low grades. I was too young to know what I wanted. Then, I went to electronic college here in the Tampa Bay (Florida) area, to study a hobby I enjoyed, and the

college indicated it might help me get a good job, but no job was forthcoming, even though I was one of three students who tied for my class valedictorian, that is, the number one spot. Even though I was

unable to get a good job, I made regular payments on my loan.

However, a few years later, figuring my 2-year vocational degree was not enough, I went back to college, and I graduated with honors and a double major from The Florida State University, hoping to pursue

genetics -another subject of which I am fond.

I achieved higher grades at Florida State than I had even during the 2 semesters I retained my “Merit Scholarship” at Hillsborough Community College, but the State of Florida did not give me

back my academic scholarship.

In plain English, what I am trying to say here is that even when I got my grades HIGHER than those who had academic scholarships, I was not given my scholarship back -the money went to students, many

of whom had LOWER grades than me, which I think was unfair, and, from a “constitutional” standpoint, a Federal Violation of Equal Protection (I was not “Equally” protected here,

since those with lower grades continued to receive academic grants.)

My total debt grew to 46 Thousand dollars, 23 Thousand of subsidized loans and 23 Thousand of unsubsidized loans. (That is, the government pays the interest on subsidized loans under some

circumstances.) I tried getting a good job in my field, but since few companies in Florida deal in genetics, any serious move I have attempted to make to obtain a job in my field would take major money

for rent (I live with my father currently), and I can afford either rent OR paying back my college loan, BUT not both -unless I want to pay only on the interest and pay on it forever!

Help!

I did not go to college to be a burger flipper, hello. I call upon My God to help me -I believe in Heaven and all, but I don’t want to be a martyr simply because greedy persons in authority

charge me interest.

In all fairness to Sallie Mae, they let me consolidate my loan and have -up to this point -continued to grant me forbearances and unemployment deferments, but the interest continues to grow,

and I don’t know, from a mathematical standpoint, how I will ever be able to pay back my loan.

When a student jumps through all the “right” hoops and yet something like this happens (and my case is not even a “horror story” -many are apparently much worse, reading

these other letters) …uh…oh! Yes, as I was saying: When a student jumps through all the “right” hoops and yet something like this happens, something is just not right,

folks.

If the “Interest” charged on my loans were no more than the rate of inflation, I could pay on the loan until it is paid off, as my pay-raises would increase in strength at the same pace as

the interest, but we know that this is not true. For this reason, it doth appear to me that “The System Is Broke.” Help…

Sincerely, and I sign with my real name to show that I am not making up this story:

Mr. Gordon Wayne Watts of Lakeland, Florida, USA, Earth.

Gordon Wayne Watts

June 2 at 10:16am

I posted a question about H.R. 5043 just now, and it's deleted - I guess you deleted it. Was my post offensive in some way? The issues surrounding that are explained on

http://GordonWatts.com/Higher-Ed-Tuition-Costs.html or

http://GordonWayneWatts.com/Higher-Ed-Tuition-Costs.html -- briefly, students used to have bankruptcy protections,

and if these standard loan protections are returned, the Federal Government will be less likely to guarantee student loans, less loans will originate, --and at a cost lower than before (Lower Tuition:

since colleges will know they can't price-gouge students without rick of bankruptcy), and this will have a "side effect" of getting Government OUT of Higher-Education. (Translation: GOOD, since

conservatives *want* the Govt out of Higher Education.)

For some reason, liberals support this too -and I suspect they view it as a free handout.

I don't want a free handout - I don't mind paying what I owe, but I don't want to be over-taxed to death, and tuition is technically a tax, since it is funding to a state-owned college in most cases

-and a college regulated by State & Federal govt is all cases.

This is a rare issue where liberals & conservatives can see eye-to-eye and agree -instead of the usual Washington 'gridlock.'

What is your take on this issue? -- And, what about my post was offensive to motivate you to delete it?

Dennis Ross

June 2 at 10:55am

Report

I toko it down because I wanted my constituents to see the post about the balanced budget hearing going on right now. Nothing offenseive, just didn't want that post mvoed down the page so far.

As for HR 5043, I do not support it. Allowing discharge in bankruptcy for student loans would cause a sharp decline in availability of loans. I also do not supoprt the federal government being the

only student loan lender, as it is now after last year.

Gordon Wayne Watts

June 2 at 11:26am

I *want* a sharp decline in the availability of student loans (ideally, I would eliminate ALL of the government's interference in the Free Market -and get the Federal Government *out* of Higher

Education altogether!)

You see, Dennis, every time Congress raises the loan limits (thus enabling students to be saddled with more debt), dishonest liberal colleges find new excuses to raise tuition (even though they're not

justified, since quality of education has actually gone down).

In the 50's US colleges were tops in the world, in tuition could be paid for by a part time job in the cafeteria over the summer.

Now-days, tuition is unbearably heavy -with some students even committing suicide -- have you ever wondered why tuition is skyrocketing much faster than inflation's rate?

Liberals who support gov't interference in the free market make unrealistically large loans available, and colleges simply charge more because they can.

But I don't see how a conservative such as you or I could support this interference in the Free Market by the Government.

If the gov't got out of guaranteeing loans (which would occur to some small degree if HR5043 passed -since bankruptcy would partly cancel out past loans -and discourage future ones from being

unrealistically large), then tuition would drop -since colleges would know they could no longer price-gouge students without repercussions.

If drug users & criminals with credit cards can get bankruptcy, why not students?

Also, when bankruptcy protections were in place for student loans just a few years ago, lender were not so irresponsible, and the default rate was not high -but when bankruptcy protections

were removed, the default rate skyrocket.

You know I'm a conservative, and I don't want to 'get out' of paying for my college education (eg getting a 'Free Handout'), but tuition is, technically, a tax, since it goes to state-owned

universities in most cases --and Federal/State regulated colleges in all cases, and students have been over taxed now for some time. You don't support this over-tax which resulted from liberals'

intefering with the free market, do you? (Hint: Colleges of the 50's were low because the gov't didn't intefere in the Free Market.)

Gordon Wayne Watts

June 2 at 2:03pm

I was a little emotional earlier --rest assured I am not mad or offended at your deleting my post. (But since I see you did delete my 'regular' email -probably afraid the attachment might infect your

computer, I will hope to gain your ear just a little longer.)

Anyhow, we've tried it the liberals' way --and all those 'Student Loans' did nothing but enable a skyrocketing tuition.

So, that's why I want to go back to the way it was: Either no loans at all -or, if there are loans, standard consumer protections (eg bankruptcy) --like it was back in the 50's --when quality of

education was high, and tuition was low.

What has, at root, caused this lending system to grow in to the predatory beast it has become, caused the schools to loose their honor in favor of greed, hurt the students, etc. is #1: the removal

of standard consumer protections from student loans & also #2: the creation of draconian collection powers. Combined, these two actions made defaults the preferable outcome for the entire lending

system, and took away the motivation to help the students from the people running the system (most importantly the people at the Department of Education).

When the people making the loans (the guarantors for the loans & even the Department of Education) lost the financial interest to help the students, but instead were given a financial incentive to

want students to default & fail, the entire system became predatory, corrupted, inflationary, etc. This is the most fundamental cause that explains the unchecked greed that came to dominate the

colleges/universities. Simply returning the standard consumer protections that were taken away (e.g., those HR 5043 reactivated) will fix this defect, and, over time, the various horrible things

that were created will go away, and this includes the raping of the students by the schools.

Government interference in the Free Market has not worked, as we see --I want the Federal Government out of Higher Ed altogether, and students who were over-taxed to be reimbursed.

Gordon Wayne Watts

June 2 at 6:16pm

I was wrong on some of what I said regarding HR 5043... and I wanted to apologise:

As I was heading out the door for lunch earlier today, Jacob Walsh, a friend I haven't heard from in years call me up because he wanted my help in helping him apologise to Alan Collinge the head

of Student Loan Justice -and it was because he changed his views on student loan bankruptcy.

I was freaked out because of the timing of this -- since I had planned, while I was at lunch, to drop off a copy of my letter to the editor that you deleted in your AOL email (you prob. deleted it

because it had an attachment --and I don't totally blame you).

Jacob has been a student loan officer for many years now, and so I took the chance to ask his opinion of the issue, so that if you and I discussed it further, I would know if I had taken a "common sense"

approach.

Jacob looked up H.R. 5043 on the computer while we talked, and he brought to my attention that this affects only private student loans -not subsidised ones, such as Stafford.

I relayed to him your concern that bankruptcy protections would chill the market, and, as you say, cause a sharp decline in availability of loans; Jacob pointed out that credit card loans are typically

on the same terms (interest, payment options, fees, etc.) as these private loans, and yet credit card loans have continued unabated -and that even someone with bad credit can find a lender.

He also pointed out that there would still be Stafford and other Federally-guaranteed loans available to student -and that they would not have any bankruptcy protections.

So, he concluded that your fears of a sharp decline in availability of loans were unfounded.

He also took a swipe at your stance on the issue, saying that you were not a 'true' republican, since he believes you are bought out by the big lenders to allow these loans to students, but I tried to

defend you on this point, saying I believed you were truly conservative. Jacob lives in Indiana, and thus not a constituent in your district, but I fear other constituents might sympathise with the

views he espoused.

Anyhow, now that I've clarified that HR 5043 doesn't touch public or backed loans, as they call them, and that even the private loans would be affected no differently than credit card loans (which are

done all the time -with no difficulty), are your fears allied?